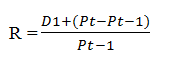

Risk and return is considered most important topic in finance and investment. The first thing that need to understand in this topic is return income. Income received on an investment plus any change in market price is known as return income. This is the formula of return income.

Where D1 = Dividend

Pt = original price

Pt-1 = Current price

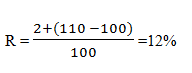

Let’s suppose if a have security original price is $ 100 and the current price is $110. The dividend received on the stock is $ 2. An investor calculates return income through the following procedure.

D1 = Dividend = 2

Pt = original price = 100

Pt-1 = Current price = 110

Put all values in formula

For instance, the important thing is return income is always in a percentage form.

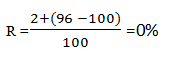

Let’s if a security current trading price is $ 96 and its original price is $100. The dividend received on a stock is $ 4. Calculate the return income of that particular security.

D1 = Dividend = 4

Pt = original price = 100

Pt-1 = Current price = 96

Put all values in formula

Risk:

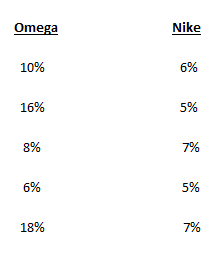

A finance expert defines risk as the variance among the actual and expected return. In simple words, the risk is uncertainty about the future. For example, there are two securities Omega and Nike. The expected returns on Omega and Nike as follows.

Above all, the risk probability is higher in Omega security. Because there are more variations in Omega.

Probability:

Occurrence chance of any event or chance of happening is called probability. Occurrence is the basic outcome of an experiment. For example, if we toss a coin there are two occurrences. Similarly, If we throw a die there should be six occurrences.

Probability Distribution:

Probability distribution is a statistical function. That defines all probable values and chances that a random variable can take within a given range. In simple words, the Chances of random variables is called probability distribution.

For example

- 10%

- 5%

- 10%

- 40%

- 20%

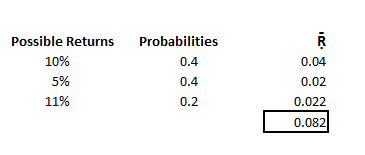

Expected return:

The weighted average of possible returns, with weights being the probabilities occurrence is called expected return. The formula of expected return is as follows

Expected return = Possible return × Probabilities

Here we assume some possible returns and probabilities. Therefore, we try to calculate expected returns.

So, there is an 8.2% expected return.

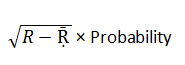

Standard Deviation:

It is a static measure of the variability of distribution around its mean. It is the square root of the variance. Therefore, we find standard deviation with the help of this formula.

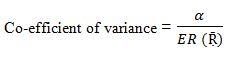

Co-efficient of Variance:

It is a statistical measure of the dispersion of the points around the mean. The co-efficient of variance determines the risk involved in a single expected unit. In other words, it is measure relative risk. We calculate the coefficient of variance in the following ways.

Certainty equivalent:

The amount of cash or equivalent somebody would require. The inevitability at a point in time to make individual indifferent between that certain amount. The expected amount is to be received with risk at the same point in time.

Risk-averse:

The term risk averse applied on an investors. The investor who requires might be a lower expected return, bearing with lower risk. In vice versa, if investor bears high risk than he should also demand for high return. This also follows an investment rule of thumb, “high risk and high profit”.

Portfolio:

A combination of different securities is called a portfolio. From a finance point of view, a combination of securities means a combination of assets, securities, bonds, etc. Investors construct portfolios according to their risk tolerance and investing objectives. Therefore, a portfolio is like a pie which is further divided into different size and nature of pieces.

Single Security Return calculate =

E(R) = R Pr. + R Pr. + R Pr.

E (R) = M∑ RjPr.j

Where = (E) R = expected return

R Pr. = Return probability

Portfolio return calculate =

E(Rp) = Wa(E)Ra + WBE(R)b + WcE(Rc) + WdE(Rd)

E (Rp) = n∑ Wi E (Ri)

Where:

E(Rp) = Expected return of portfolio

W = weight of security

Types of risk:

As we already discussed above that risk is uncertainty about the future. Generally, there are two types of risk considers in finance.

Systematic risk:

It is part of the total risk that is cause by different factors. These factors are not in the control to any specific individual, and a company. This is cause by external factors and not controllable for a firm. This risk exists on all assets, stocks, and securities. As a result, we call them non-diversified risk. It is not possible to eliminate this risk through efficient diversification of a portfolio. The common example of systematic risk is changes in tax laws, market risk, purchasing power risk etc.

Unsystematic risk:

The systematic risk is also known as diversified risk. It is the risk of a specific firm, industry. This risk can be eliminated through the efficient use of resources, better management, and diversification of a portfolio. For example one of the prestigious textile organization is working as usual. But suddenly due to some misunderstandings, or something else. The staff go to strike. Now, this is an unplanned risk, happen suddenly and also causes widespread disruption. The stock prices of this textile organization should fall due to this strike. But still, this is controllable through dialogue and well handling. So, we may call this risk as unsystematic risk.

Diversification:

Diversification is the process to manage investment in a well-organized way. Invest in different sectors instead of anyone to eliminate and minimize the risk. In diversification, an investor invests in different sectors with different weights.

Capital asset pricing model (CAPM):

The capital asset pricing model is the relationship between expected risk and expected return based on the market beta. CAPM shows that the expected return on a stock. In addition, expected return is the combination of risk-free return risk premium. The risk premium is based on the beta of that stock. The formula of CAPM is given below.

Ra = Rf + [× (Rm – Rrf)]

Where:

Ra = Expected return on a stock

Rf = Risk-free rate

Ba = Beta of security

Rm = Expected market return

Risk Premium = Rm – Rf

Question No. 1:

Use capital asset pricing model (CAPM). To estimate the expected return for the shares of NCK.

(i) your case company Nick Scali (NCK)

(ii) A hypothetical company with a beta of 1.60. When calculating, use the yield to maturity of a 10-year Australian Government bond on 1 April 2020 as a proxy for the risk-free rate (RF). Suppose the market risk premium is 5.50% and use your case company’s most recent 5-year beta.

(iii) Using the data from part (ii). Estimate portfolio expected return and beta. Assuming a portfolio with 70% invested in your case company. The remainder invested in the hypothetical company

- Unlock free of cost solution of this question on quality assignment help sample page. Click here

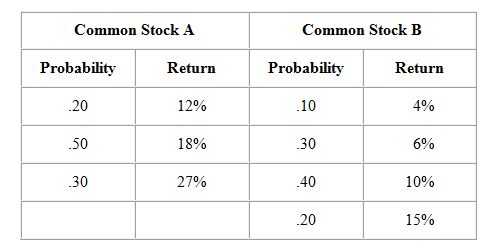

Question No. 2:

(a) Friedman Manufacturing, Inc. has prepared the following information regarding two investments under consideration. Which investment is better, based on risk (as measured by the standard deviation) and return?

(b) “ More can be said about risk, especially as to its nature. When we own more than one asset in our investment portfolio.” Define risk and explain how risk is affect. If we diversify our investment by holding a variety of securities?

- Unlock free of cost solution of this question on quality assignment help sample page. Click here

If you still have any confusion regarding any financial help. Please don’t hesitate to contact us. Quality assignment help experts are ready to help you. Click here